EU Commission issues tax simplification package: Tax Omnibus and DAC Recast

On 24 June 2026, the EU Commission published two legislative proposals aimed at simplifying EU tax rules, reducing compliance burdens for businesses and strengthening the competitiveness of the Internal Market: the direct taxation Omnibus (Tax Omnibus) and the Recast of the Directive on Administrative Cooperation (DAC Recast).

Tax Omnibus

The Tax Omnibus amends six existing Directives. Below is a summary of the main proposed measures, highlighting the potential impact for Luxembourg corporate taxpayers.

Interest and Royalties Directive (IRD) — Council Directive 2003/49/EC

The proposal broadens and simplifies access to the IRD exemption from withholding tax on intra-EU interest and royalty payments.

Removal of minimum holding requirement: the “associated company” concept, which currently requires a minimum participation of at least 25%, is removed. All intra-EU interest and royalty payments, irrespective of the participation level between payer and payee, will be eligible for the withholding tax exemption.

Introduction of safeguard to prevent situations of double non-taxation: where the recipient of the interest or royalty payment is established in a jurisdiction that does not levy corporate income tax or applies a zero tax rate, the source Member State must either levy withholding tax or deny deductibility. This safeguard does not apply to recipients covered by the Pillar 2 framework.

Removal of upfront procedures: prior authorisation and administrative procedures are removed. As a general rule, eligibility is self-assessed by the taxpayer, subject to ex post controls and anti-abuse rules (including beneficial ownership rules). Where the paying company cannot determine eligibility in advance (e.g. for publicly traded securities), FASTER fast-track procedures or standard domestic refund mechanisms within a reasonable time will apply.

Other points: the proposal clarifies that the IRD covers payments attributable to a permanent establishment regardless of local tax deductibility, and updates the list of eligible company forms in the Annex (with a Commission delegated act power for future updates).

Luxembourg perspective

As a general rule, Luxembourg levies no withholding tax on interest and royalties paid to EU resident companies, save on profit-sharing bonds. The most relevant change would therefore be the proposed safeguard measure, as the current safeguard only denies tax deductibility for interest and royalties due to a related party established in a country or territory appearing on the EU list of non-cooperative jurisdictions.

Parent-Subsidiary Directive (PSD) — Council Directive 2011/96/EU

The PSD exempts dividends and profit distributions paid by subsidiaries to parent companies in other Member States from withholding tax and eliminates double taxation of such income at the level of the parent company. The proposal includes the changes described below.

Removal of minimum holding requirement: the current 10% minimum participation threshold is abolished (as is the optional minimum two years holding period). All intra-EU dividend and profit distributions are eligible for the withholding tax exemption and participation exemption regardless of the participation level. The option for Member States to deny deduction of charges or losses connected to the holding of participations is limited to cases where the participation is 10% or more.

Extension to pension institutions: the PSD’s personal scope is extended to pension institutions regardless of legal form. Profit distributions received by pension institutions from companies in other Member States will be exempt from withholding tax via a derogation from the PSD’s subject-to-tax condition.

Removal of upfront procedures: prior authorisation procedures are eliminated and replaced by ex post controls and the application of anti-abuse rules by Member States, including rules on beneficial ownership. Similarly to the IRD, when the taxpayer will not be able to verify eligibility at the time of payment, either FASTER procedures or domestic refund procedures within a reasonable time will apply.

Other points: the proposal updates the Annex of eligible company forms (with a Commission delegated act power for future updates).

Luxembourg perspective

The current Luxembourg participation exemption regime (for the withholding tax exemption for dividend distributions and the participation exemption for dividends) requires a minimum participation threshold of 10% or an acquisition price of at least EUR 1.2 million, as well as a minimum retention period of 12 months, or a commitment to do so. Luxembourg would therefore need to amend the relevant provisions to align with the proposed measures, if finally agreed. It remains to be seen how these changes would impact the participation exemption applicable to liquidation proceeds and capital gains received.

Anti-Tax Avoidance Directive (ATAD) — Council Directive (EU) 2016/1164

ATAD is amended to extend its material scope and include the full expensing of certain research and development (R&D) expenditure.

New R&D expensing framework: a new EU-wide minimum standard is introduced for the tax treatment of capital expenditure on plant, machinery and other tangible assets used directly for R&D or to support R&D facilities. Taxpayers may immediately deduct qualifying expenditure in the tax period incurred or elect to do so in any of the four subsequent tax periods. Assets must be used exclusively for R&D for a minimum of three years. Rules on withdrawal of the allowance and balancing charges where assets are disposed of, demolished or cease to be owned are also introduced.

Interest limitation rule amendments:

- 30% EBITDA amount made mandatory (removing Member States’ option to set lower thresholds).

- EUR 3 million safe harbour becomes mandatory, with annual inflation indexation.

- Low-risk third-party borrowing (from non-associated lenders, not on-lent within the group) excluded from the limitation.

- Option to exclude standalone entities removed.

- The list of financial undertakings (that are excluded from the scope of the rule) is updated to reflect developments in EU financial regulation, and ensure the rule remains fit for purpose. In particular, AIFs are removed from the list, and the proposal would add other entities, such as insurance or reinsurance SPVs, payment or electronic money institutions, and crowdfunding or cryptoasset service providers.

- No interest limitation will apply to a taxpayer when its EBITDA is reduced by 50% in a tax year.

- Group escape rule and carry-forward mechanism both made mandatory.

- Temporary exclusion for eligible defence-related borrowing introduced for the first five tax years following entry into force.

- Long-term public infrastructure exclusion broadened to all long-term public-benefit projects.

- New “no-divergence” clause would prohibit Member States from maintaining or introducing any national rule on the same subject matter that diverges from the interest limitation rule of the ATAD as amended.

GAAR update: the general anti-abuse rule is updated to expressly cover all taxes to which companies are subject, including withholding taxes and Pillar 2 top-up taxes.

CFC rule simplification:

- Taxpayers within scope of the Pillar 2 framework are exempted from controlled foreign companies (CFC) charges to eliminate overlap, unless the group is headquartered in a jurisdiction which operates a qualified “side-by-side” regime and the low-taxed controlled foreign subsidiary is not subject to qualified domestic top-up tax or, where it is subject to a qualified domestic top-up tax, a refund or direct or indirect financial benefit is granted in relation to that tax.

- SMEs are also exempted.

- Model B is abolished, as it is considered to overlap with transfer pricing rules. Model A (broadly, the inclusion of non-distributed passive income from shell companies) becomes the sole applicable method.

- The passive income de minimis exemption and financial undertaking exemption become mandatory.

- A “no-divergence” clause is also introduced (similarly to the interest limitation rules).

Amendment to hybrid mismatch rules: the imported mismatch rules are removed.

Luxembourg perspective

R&D costs are in general fully tax deductible, either as expenses or as depreciation. Luxembourg may need to adapt the relevant provisions to align with the proposed measure.

If the proposed rules are adopted, Luxembourg will need to amend several provisions of its interest limitation rules, which will include removing the exemptions for standalone entities and AIFs.

The removal of AIFs from the list of financial undertakings excluded from the interest limitation rule warrants specific attention for Luxembourg debt funds. Under the current ATAD framework (as implemented in Luxembourg law), AIFs are listed as financial undertakings and are therefore entirely excluded from the 30% EBITDA-based interest limitation rule. Under the proposal, Luxembourg AIFs that are subject to corporate income tax and that have exceeding borrowing costs would become subject to the interest limitation rule, unless the entity qualifies for another exclusion, such as the new low-risk third-party borrowing exclusion (which requires that the loan is not on-lent within a group).

The timing for this measure is material: if adopted, Member States must implement the measures by 31 December 2028 and apply them from 1 January 2029. Luxembourg AIFs and their sponsors should begin assessing the potential impact on existing fund structures now, in particular for funds with long investment periods that extend beyond 2029.

Luxembourg will also need to amend its CFC rules, in particular to replace Model B with Model A, as well as the hybrid mismatch rules. The GAAR is not expected to be (significantly) modified.

Tax Merger Directive (TMD) — Council Directive 2009/133/EC

The TMD provides for tax-neutral treatment of cross-border reorganisations (mergers, divisions, transfers of assets, exchanges of shares). The proposal updates its scope to align with recent EU company law developments.

New reorganisation types: two transaction types introduced by the Mobility Directive (Directive (EU) 2019/2121 amending Directive (EU) 2017/1132). The “simplified merger” and the “division by separation” are added to the TMD’s definitions and will now benefit from the tax neutrality regime.

Cross-border conversions: a new chapter extends the TMD’s tax neutrality principles to all cross-border conversions (including at minimum the transfer of a company’s registered office), which were previously only available to European companies (SE) and European cooperative companies (SCE). Capital gains on assets of a converting company will be deferred until actual disposal, provided the company remains tax resident in the departure Member State, or retains a permanent establishment connected to the relevant assets in the departure Member State.

Other points: the proposal updates the Annex of eligible company forms (with a Commission delegated act power for future updates).

Luxembourg perspective

If the proposed measures are adopted, Luxembourg will need to amend the corporate reorganisation provisions of the Income Tax Law to align with the proposed measures.

FASTER Directive — Council Directive (EU) 2025/50

FASTER provides for standardised fast-track procedures for relief at source or quick refund of withholding tax levied on dividends and interest from publicly traded securities.

Under the current provisions, Member States may deny access to the standardised fast-track procedures where a full exemption from withholding tax is claimed. This would de facto prevent the benefit of the FASTER procedures for refund from applying to payments which are eligible for exemption under the extended scope of the IRD and PSD. For this reason, the proposal adjusts the scope of FASTER, to ensure that it covers refunds under the IRD/PSD.

Luxembourg perspective

Luxembourg has not yet implemented the FASTER Directive (implementation deadline is 31 December 2028 with application from 1 January 2030).

For investment funds, and in particular for Luxembourg-domiciled funds holding publicly traded debt or equity securities issued by entities in other Member States, the extended FASTER procedures will be the primary mechanism through which IRD/PSD withholding tax relief – see above – can be claimed where the paying company cannot determine the investor’s eligibility at the time of payment. The proposed measures are therefore particularly relevant for debt funds holding publicly traded bonds.

Dispute Resolution Mechanism Directive (DRM) — Council Directive (EU) 2017/1852

The DRM provides mechanisms for resolving cross-border double taxation disputes. The proposal introduces targeted amendments to streamline procedures and broaden taxpayer access.

DAC Recast

The proposal to recast Council Directive 2011/16/EU on administrative cooperation in the field of direct taxation (DAC) consolidates the original DAC and its eight successive amendments (DAC 1 through DAC 9) into a single, streamlined legal act and introduces targeted simplification measures aimed at reducing compliance costs for businesses and improving the efficiency of tax administrations across the EU.

Below is a summary of the main proposed measures.

DAC 6 (reportable cross-border arrangements)

- Entities subject to the Pillar 2 rules are carved out from DAC 6 reporting (provided the ultimate parent entity is not located in a jurisdiction with a qualified side-by-side regime, unless the relevant participant is subject to a qualified domestic top-up tax and no refund/financial benefit applies).

- The Category A generic hallmarks (related to a confidentiality clause, contingent fees or standardised documentation and/or structure) are deleted entirely.

- Hallmark C1(b)(ii) now refers to deductible cross-border payments made to a recipient resident in a jurisdiction on the “EU blacklist” (the reference to the OECD list is deleted).

- The reporting deadline is extended from 30 days to 90 days following the first concrete step of implementation. The two other triggering events of a reportable arrangement (i.e. when the arrangement is made available for implementation or is ready for implementation) are deleted.

DAC 7 (digital platform)

- The activity threshold for sales of goods on digital platforms (currently 30 transactions per year) is removed, and the monetary threshold is raised from EUR 2,000 to EUR 3,000 per year.

DAC 4/DAC 9 (Country-by-Country Reporting (CbCR) and Pillar 2 notifications)

- The proposal merges the notification obligations under CbCR (DAC 4) and for central filing of the Pillar 2 top-up tax information return (DAC 9) into a single notification, filed in a common template by the last day of the MNE group’s fiscal year.

TIN Verification Tool

- A new centralised digital tool for verifying Taxpayer Identification Numbers (TINs) will be developed by the EU Commission. It will be mandatory for tax administrations and optional for reporting entities.

Mandatory automatic exchange of information

- The life insurance products category is removed from mandatory automatic exchange.

- All six remaining income and asset categories must now be mandatorily exchanged.

- The concept of “available information” is broadened to include information held by other public authorities at national level, including AML registers and the new interconnected real estate beneficial ownership register.

Next steps

Both proposals will be submitted to the EU Parliament for consultation and to the Council of the EU for adoption, requiring unanimous agreement among the Member States.

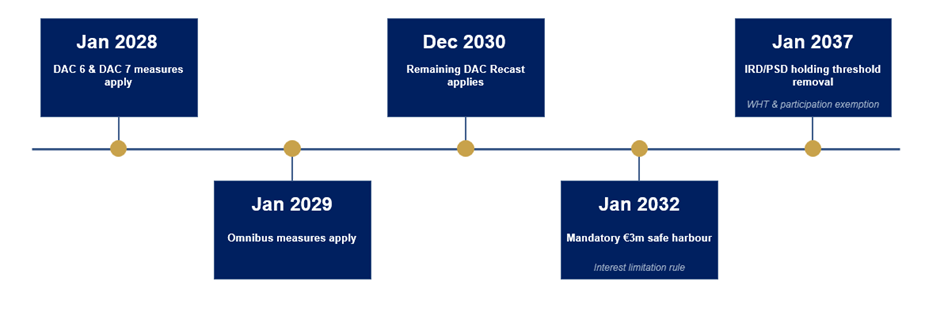

If adopted, Member States must implement the proposed Tax Omnibus measures by 31 December 2028 and apply them from 1 January 2029. However, most of the above IRD and PSD changes (in particular, removal of the minimum holding requirement for application of the withholding tax exemption and/or the participation exemption) would only apply from 1 January 2037. The mandatory EUR 3 million safe harbour with annual inflation indexation in the interest limitation rule would only apply from 1 January 2032.

With respect to the DAC Recast, if adopted, Member States must implement part of the proposed measures (including in particular the DAC 6 measures) by 31 December 2027 and apply them from 1 January 2028. The remaining DAC Recast provisions must be implemented by 31 December 2029 and apply from 1 December 2030.

How we can help

The Tax partners and your usual contacts at Arendt & Medernach are at your disposal to further assess and advise on the impact of the proposals on your operations.

Contacts

Alain Goebel

Partner

Dr. Philipp Jost

Partner

Thierry Lesage

Co-Chair, Partner

Vincent Mahler

Partner

Stéphanie Maschiella

Partner

Jan Neugebauer

Partner

Yves Philippart de Foy

Partner