Implementation of CSRD into Luxembourg law: expanded sustainability reporting obligations for Luxembourg and foreign undertakings

Bill of law 8370 implementing the CSRD in Luxembourg will bring significant changes to the reporting obligations of in-scope undertakings in order to provide a comprehensive overview of the social, environmental, and governance impacts of these undertakings, contributing to greater transparency and accountability.

On 29 March 2024, bill of law 8370 (Bill of Law) was submitted to the Luxembourg Chamber of Deputies to implement Directive (EU) 2022/2464 as regards corporate sustainability reporting (Corporate Sustainability Reporting Directive or CSRD), as well as the related Delegated Directive (EU) 2023/2775 as regards the adjustments of the size criteria for micro, small, medium-sized and large undertakings or groups (Delegated Directive).

The CSRD, which entered into force on 5 January 2023, was adopted with the objective of creating a common reporting framework for sustainability information by modernising and strengthening the rules concerning the environmental, social and governance information on which in-scope companies must report. In addition to the European Sustainability Reporting Standards (ESRS), adopted on 31 July 2023, the CSRD aims to ensure that the relevant information included in a dedicated section of the annual management report of in-scope companies must be consistent, relevant, comparable, reliable and easy to access.

The Bill of Law aims to amend several national laws, including in particular:

- the law of 19 December 2002 on the Trade and Companies Register and the accounting as well as annual accounts of companies,

- the law of 10 August 1915 on commercial companies,

- the law of 17 June 1992 relating to the annual and consolidated accounts of credit institutions,

- the law of 8 December 1994 relating to the annual and consolidated accounts of insurance and reinsurance companies,

- the law of 5 April 1993 on the financial sector,

- the law of 7 December 2015 on the insurance sector and

- the law of 23 July 2016 concerning the audit profession.

1. Scope of application and timeline

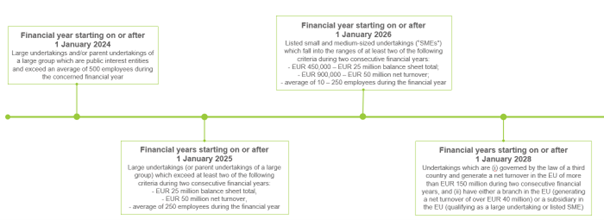

The following undertakings fall within the scope of the CSRD and must comply with the new reporting obligations:

- as from financial years starting on or after 1 January 2024: large undertakings and/or parent undertakings of a large group which are public interest entities (e.g. listed undertakings, credit institutions and insurance undertakings) and exceed an average of 500 employees during the concerned financial year

- as from financial years starting on or after 1 January 2025: large undertakings (or parent undertakings of a large group) which exceed at least two of the following criteria during two consecutive financial years:

- EUR 25 million balance sheet total;

- EUR 50 million net turnover;

- average of 250 employees during the financial year

3. as from financial years starting on or after 1 January 2026: listed small and medium-sized undertakings (SMEs) which fall into the ranges of at least two of the following criteria during two consecutive financial years:

- EUR 450,000 – EUR 25 million balance sheet total;

- EUR 900,000 – EUR 50 million net turnover;

- average of 10 – 250 employees during the financial year; and

as from financial years starting on or after 1 January 2028, undertakings which are (i) governed by the law of a third country and generate a net turnover in the EU of more than EUR 150 million during two consecutive financial years, and (ii) have either a branch in the EU (generating a net turnover of over EUR 40 million) or a subsidiary in the EU (qualifying as a large undertaking or listed SME).

4. as from financial years starting on or after 1 January 2028, undertakings which are (i) governed by the law of a third country and generate a net turnover in the EU of more than EUR 150 million during two consecutive financial years, and (ii) have either a branch in the EU (generating a net turnover of over EUR 40 million) or a subsidiary in the EU (qualifying as a large undertaking or listed SME).

However, listed SMEs may decide to opt out of their reporting requirements for a further two years, i.e. reporting in 2029 for the financial year starting on or after 1 January 2028.

In addition to the criteria regarding size, only Luxembourg undertakings formed as a société anonyme (SA), société en commandite par actions (SCA), société à responsabilité limitée (SARL) and société cooperative, as well as société en nom collectif (SNC) and société en commandite simple (SCS), if all the members having unlimited liability in the latter are limited liability companies (i.e. are either an SA, SCA, SARL or société cooperative), fall within the scope of the CSRD. However, according to the Bill of Law, Luxembourg includes undertakings formed as sociétés européennes (SE) in the scope of the CSRD as regards the corporate form criteria, provided that the other criteria are met.

With regard to the banking and insurance sectors, it must be noted that the net turnover criterion has been adapted with regard to the activities of credit institutions and insurance undertakings:

- for credit institutions, the adapted concept of net turnover includes “banking income” (referring, for example, to interest and similar income, income from securities, commissions received, income from financial transactions), and

- for insurance undertakings, the adapted concept of net turnover includes “gross premiums”.

2. General reporting obligations

Undertakings that fall within the scope of the CSRD must include in their management report a dedicated section that outlines information necessary to understand:

- the undertaking’s impact on sustainability matters, and

- how sustainability matters affect the undertaking’s development and performance.

Therefore, in accordance with the double materiality principle, undertakings must disclose information presenting:

- the risks and opportunities arising from social and environmental issues, and

- the impact of their activities on people and the environment.

This information needs to be understandable, relevant, verifiable, comparable and represented in a faithful manner. The report must include information about the undertaking’s own operations and about its value chain, including its products and services, business relationships and supply chain.

3. Particularities of the Bill of Law

3.1 Commercially sensitive information

The CSRD provides Member States with the option to, under certain circumstances, allow undertakings to exclude commercially sensitive information from the sustainability report, such as information relating to impending developments and matters under negotiation, especially in cases where disclosing this information would seriously prejudice the commercial position of the undertaking. Luxembourg exercises this option in the Bill of Law.

3.2 Assurance on sustainability information

In general, a statutory auditor or an audit firm will carry out the limited assurance on sustainability information to enhance its reliability. However, the CSRD gives Member States the option to accredit independent assurance service providers (IASPs) to express their opinion and conclusions on sustainability information, although this is not currently provided for in the Bill of Law to be implemented by Luxembourg. Member States that exercise the option to introduce IASPs must also exercise the option permitting separate statutory auditors/audit firms to carry out the audit of financial statements and assurance of sustainability reporting.

3.3 Sanctions

Companies that fail to comply with the CSRD may be subject to administrative sanctions by the CSSF and to criminal sanctions. In addition, the Bill of Law emphasises that it should be noted that a failure to comply with such requirements may result in reputational risks, market risks and operational risks, such as an interruption of access to funding sources.

4. Next Steps

The CSRD requires that Member States implement the Directive into national law by 6 July 2024.

The Bill of Law is currently under review by, inter alia,the Luxembourg Council of State and the Chamber of Deputies and is expected to soon be discussed in public session. In view of the fast-approaching deadline for the implementation of the CSRD, it can be expected that the legislative process will accelerate and that the law will thus be adopted in the upcoming months.

5. Noteworthy for Private Equity firms

It is interesting to note that certain exceptions and exclusions that were initially applicable only to the obligation to report on financial obligations (on a stand-alone and/or consolidated basis) may, under certain conditions, now apply also to the corporate sustainability reporting. This may be particularly interesting for Luxembourg-based private equity firms where Luxembourg law offers significant flexibility.

How we can help

Do not hesitate to contact our experts for help with meeting the challenges posed by the implementation of CSRD.

Contacts

Emmanuelle Mousel

Partner

Clara Bourgi

Counsel

Antoine Peter

Director

Philippe Harles

Partner

Dino Serafini

Counsel